Business credit is a crucial aspect of any successful company. It refers to the financial history of a business, indicating its ability to repay debts and fulfill financial obligations. Similar to personal credit, business credit is evaluated through a credit report that includes a credit score based on payment history, debts, credit utilization, and other relevant business information. However, it is important to note that business credit is separate from a business owner’s personal credit profile.

Understanding Business Credit

Business credit is essential when a company needs to borrow funds from a lender. Lenders rely on a business’s creditworthiness to assess the risk associated with granting a loan. For instance, if a business requires additional working capital to support its operations, it may apply for a cash flow loan. During the loan application process, lenders will review the business credit report to evaluate the financial health of the company.

While personal credit reports are provided by the three main credit bureaus—Experian, Equifax, and TransUnion—business credit reports are generated by different credit bureaus, such as Experian Commercial, Equifax Small Business, and Dun & Bradstreet. To obtain a business credit report from Dun & Bradstreet, businesses must register with the agency and receive a unique D-U-N-S Number, which lenders can reference.

The Importance of Business Credit

Maintaining good credit for your business offers several benefits. It increases the likelihood of loan approvals, enables negotiation for lower interest rates, and provides leverage in contract negotiations. Building business credit is vital for long-term success, as it allows you to separate your personal finances from your business’s financial obligations.

Building Business Credit

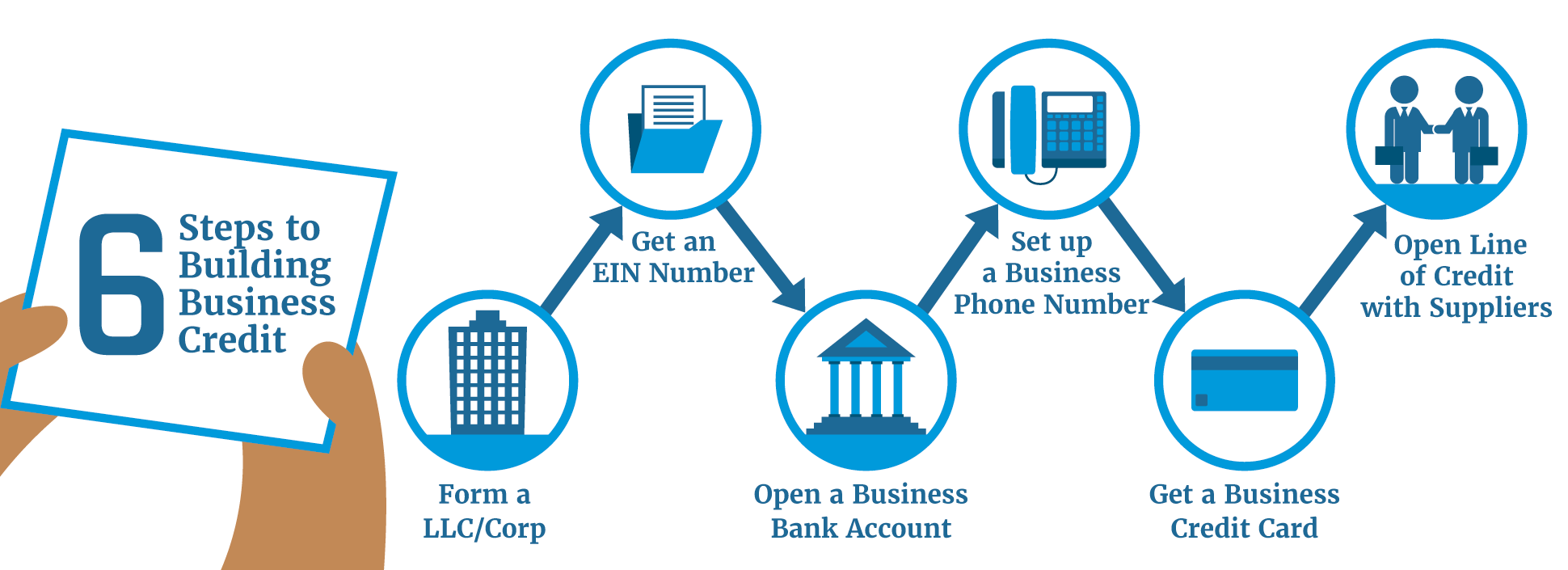

To establish a favorable business credit score, it is crucial to follow certain steps. Firstly, ensure that your business is legally registered as a separate entity, such as a limited liability company (LLC) or a corporation. Secondly, obtain an Employer Identification Number (EIN) from the IRS, which serves as a unique identifier for your business when applying for credit and filing tax returns. Additionally, opening a business bank account helps to separate personal and business finances.

Once your business is established, you can start building credit by applying for credit products specifically designed for businesses. These may include business credit cards, lines of credit, term loans, vendor credit, and service credit. Each of these products contributes to your business’s credit history and can help improve your credit score over time.

Types of Business Credit

There are several types of business credit available to meet different financial needs. Understanding these options can help you make informed decisions when seeking credit for your business:

1. Business Credit Card

A business credit card is a convenient tool for establishing and building business credit. Similar to personal credit cards, it sets a credit limit that can be used for business expenses. Paying off the balance each month demonstrates responsible credit management and can positively impact your credit score.

2. Line of Credit

A line of credit is a flexible credit option that provides funds that can be used as needed. With a line of credit, you only pay interest on the amount of credit you utilize. This type of credit is particularly useful for managing cash flow fluctuations and short-term financing needs.

3. Term Loan

A term loan is a traditional loan offered by banks or other lenders. It allows businesses to borrow a specific amount and repay it in installments over a predetermined period. Term loans are commonly used to finance long-term investments, such as equipment purchases or business expansions.

4. Vendor Credit

Vendor credit enables businesses to purchase goods or services from suppliers and pay for them at a later date. This arrangement allows businesses to manage cash flow by financing their purchases. Building a positive payment history with vendors can contribute to a stronger business credit profile.

5. Service Credit

Service credit involves utility bills and other services, such as internet and phone lines, that are registered under the business’s name. Consistently paying these bills on time demonstrates financial responsibility and can positively impact your business credit score.

Monitoring Business Credit

Once you have established business credit, it is crucial to monitor your credit report and score regularly. Regular monitoring allows you to identify any errors or discrepancies that may negatively impact your credit profile. By addressing these issues promptly, you can maintain a healthy business credit history.

Conclusion

Understanding business credit and how it works is vital for any business owner. Building and maintaining a strong business credit profile provides numerous benefits, such as increased access to financing, lower interest rates, and improved negotiation power. By following the steps outlined in this article, you can establish and nurture a positive business credit history, setting your business up for long-term success.

Remember, business credit is separate from personal credit, and it is important to keep these two aspects of your financial life distinct. Regularly monitoring your business credit and addressing any issues promptly will help you maintain a healthy credit profile and optimize your business’s financial opportunities.